Fact checking USA Today's ACA news report

Some major players, such as Anthem, plan to no longer offer coverage in many places next year in part because of uncertainty about federal policy. But Centene, another insurer, is expanding its coverage areas.

So its not really a problem?

Facts:

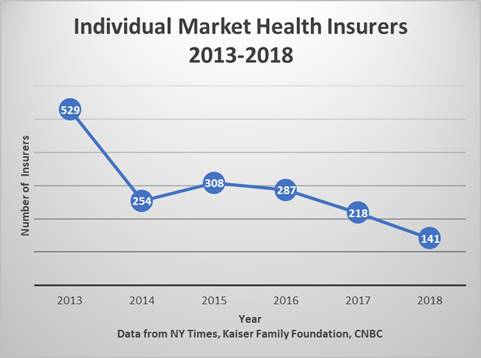

In two more years, there will be no Individual Market Health Insurers in the United States! Draw the trend line yourself!

For 2018, about 55% of counties have zero to two insurers. Dozens of counties, including almost the entire state of Nevada have zero insurance companies now. The ACA requires all individuals to buy insurance but it did not require that insurance companies actually sell insurance. By law, residents in areas without any available insurance must pay the “shared responsibility tax penalty” fee for not having insurance that is not available to them. Seriously.

USA Today spins the loss of insurance companies as “not a problem” and merely a pesky detail that, well, is not a problem. This is an example of media propaganda.

Source: Obamacare repeal is dead for now. What could that mean for you?

USA Today goes on with the following meme which is not the root cause problem, as they imply it is:

The pool of people using the exchanges has been sicker and older than anticipated, which leads to higher premiums and fewer insurance companies willing to participate. One reason there aren’t more younger, healthier people buying insurance on the exchange is because of one of the ACA’s most popular provision: the requirement that insurers let young adults stay on their parents’ plans until age 26. The Obama administration also allowed people to keep their pre-ACA plans longer than originally anticipated, which kept some healthier people from moving to the marketplace. And insurers complain that the ACA’s penalties for not having coverage are too lenient, and that it’s too easy for people to enroll only when they anticipate needing care.

All of the above statements are true – but the “young, healthy” people components line is a fake argument adopted as fact by the fiction news media.This is called an “error of omission”. It is not lying, it is just leaving out important details.

It is true that fewer “young, healthy” people signed up for ACA plans than were forecast by the original models. But that is not the reason “the pool of people using the exchanges has been sicker and older than anticipated”.

The reason was by DESIGN: By specific design of the ACA, very large numbers of very sick people were dumped into the small individual market risk pool. Their costs are now shared exclusively with other members of the small individual risk pool, causing all individual market insurance premiums to sky rocket.

No one wants to admit that the ACA contains this fatal design defect. Fatal? Yes. 2017 has fewer ACA enrollees than 2016. (In fact, 2017 has less than half the number of enrollees that were forecast for 2017.) As premiums sky rocketed, fewer people enrolled, resulting in the risk pool becoming more sick and more expensive. This is the “death spiral”.

Why did this happen?

High Risk and Pre-Existing Condition Patients

- Prior to the ACA, 35 states ran their own high risk insurance pools for people with very expensive health conditions. Post ACA, all but one of these state pools was merged into the ACA individual market. Literally, a large group of sick and expensive patients was dumped into the individual market risk pool. (New Mexico has not forced their high risk patients into the ACA individual market for fears that it will cause insurance premiums to sky rocket for everyone else.)

- How expensive are these patients? While these high risk patients made up just 2% of all the individual market, the average of the top half of claims in 2012 was $225,000 per person. The only people who pay for these highly expensive patients are the members of the individual market risk pool.

- Pre-ACA, an estimated 25% of the uninsured had pre-existing conditions. A primary purpose of the ACA was that pre-existing condition exclusions would go away. By definition, a pre-existing condition is a higher risk patient having higher costs. Where did these people end up? They and their high costs were dumped into the individual market risk pool.

The ACA turned the individual market into a bigger high risk, high cost insurance pool with average premium hikes of more than 100% from 2014 to 2017 (according to the US Department of Health and Human Services) with 3 states seeing hikes of more than 200%.

Thus, the ACA dumped a large group of very expensive patients into the individual market risk pool. Who pays for these high costs? As of 2017, ONLY THE OTHER MEMBERS OF THE INDIVIDUAL RISK POOL. There are not enough young people to offset these costs and young people pay far less in premiums than those over age 43. Thus, the “young and healthy” meme is largely bogus. Reporters support the ACA and do not want their readers to know the ACA contains serious defects. Therefore, they wave their hands and blame a lack of young people enrolled.

About half of those in the pool get government subsidies that hide all rate increases (taxpayers pick up the tab). The other half have to absorb all of the costs of covering these high risk patients, hence 100% to 200% price hikes in 3 years. (The actual number of unsubsidized is far greater than half – a subject for another post.)

(Full details and references are here.)

If Democrats and Republicans want to improve the marketplaces, what could they do?

Besides ending the dispute over the cost-sharing subsidies, lawmakers could also continue one of the other industry supports which was only supposed to be temporary. That program essentially subsidies the cost of the sickest customers, which would reduce premiums. Experts have proposed many other changes including expanding premium subsidies, giving insurers incentives to sell plans in counties that would otherwise lack coverage, and making families eligible for premium subsides if plans offered by an employer aren’t affordable.

Good God. The only way to make the ACA work is to subsidize insurance companies and subsidize more people? That is the definition of a failed market and a failed government program.

These problems are solvable without mass subsidies. To learn more, read my paper.

Unfortunately, since 2009, there have been close to zero complete and honest news reports about the ACA, which contributes greatly to why we are now in this mess of tens of millions either not having insurance or not being able to afford health insurance. (About 10 million unsubsidized individual market consumers, 6.5 million paying the “shared responsibility tax penalty” and 21.5 million who are still uninsured and not paying the tax penalty – that’s 38 million people. But that’s a trifling little number that we don’t need to worry about says USA Today! CNBC published the same nonsense this past week – hinting this was a “planted” PR story. I will address that story another day.)

USA Today has so many errors and logical fallacies going on that they have morphed into a fiction news service. Is their fiction writing due to propaganda or simply incompetence? We have no idea.

Sadly, no one gives a shit except for the tens of millions who have been screwed. And which the media intentionally ignore.